https://cornerstonelaw.us/wp-content/uploads/2024/05/10.5-Notice-Individual-Example-scaled.jpg

2560

1978

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

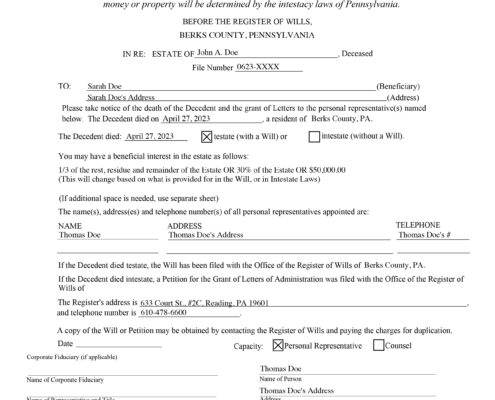

Cornerstone Law2024-06-10 12:22:162025-07-01 11:59:39Completing Certification of Notices (10.5s) in the Estate Process

https://cornerstonelaw.us/wp-content/uploads/2024/05/10.5-Notice-Individual-Example-scaled.jpg

2560

1978

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2024-06-10 12:22:162025-07-01 11:59:39Completing Certification of Notices (10.5s) in the Estate Process https://cornerstonelaw.us/wp-content/uploads/2023/05/Will-reading-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2023-05-09 09:52:282024-11-13 11:10:07When is the Reading of the Will?

https://cornerstonelaw.us/wp-content/uploads/2023/05/Will-reading-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2023-05-09 09:52:282024-11-13 11:10:07When is the Reading of the Will? https://cornerstonelaw.us/wp-content/uploads/2022/12/Estate-sunset-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-12-29 15:00:082023-05-04 16:02:05Am I Responsible for My Parent's Debts?

https://cornerstonelaw.us/wp-content/uploads/2022/12/Estate-sunset-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-12-29 15:00:082023-05-04 16:02:05Am I Responsible for My Parent's Debts? https://cornerstonelaw.us/wp-content/uploads/2022/11/Signing-short-certificate.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-11-21 15:33:152023-05-04 16:18:20What can I do with a short certificate?

https://cornerstonelaw.us/wp-content/uploads/2022/11/Signing-short-certificate.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-11-21 15:33:152023-05-04 16:18:20What can I do with a short certificate? https://cornerstonelaw.us/wp-content/uploads/2022/09/Right-of-Sepulchre-sunset-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-09-08 14:42:022023-05-15 17:06:33The Right of Sepulchre

https://cornerstonelaw.us/wp-content/uploads/2022/09/Right-of-Sepulchre-sunset-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-09-08 14:42:022023-05-15 17:06:33The Right of Sepulchre https://cornerstonelaw.us/wp-content/uploads/2022/09/Guardianship-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-09-04 11:12:432024-11-13 13:57:59Guardianship: When Loved Ones Cannot Care for Themselves

https://cornerstonelaw.us/wp-content/uploads/2022/09/Guardianship-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-09-04 11:12:432024-11-13 13:57:59Guardianship: When Loved Ones Cannot Care for Themselves https://cornerstonelaw.us/wp-content/uploads/2022/09/Family-settlement-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-09-01 08:52:422024-11-13 14:04:47Reaching Family Settlement Agreements in Estates

https://cornerstonelaw.us/wp-content/uploads/2022/09/Family-settlement-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-09-01 08:52:422024-11-13 14:04:47Reaching Family Settlement Agreements in Estates https://cornerstonelaw.us/wp-content/uploads/2022/08/College-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-08-19 16:36:232024-11-13 13:51:23Does my College Aged Student Need a Power of Attorney?

https://cornerstonelaw.us/wp-content/uploads/2022/08/College-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-08-19 16:36:232024-11-13 13:51:23Does my College Aged Student Need a Power of Attorney? https://cornerstonelaw.us/wp-content/uploads/2022/08/POA-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-08-10 09:17:292024-11-13 11:15:57What is a Power of Attorney in Pennsylvania?

https://cornerstonelaw.us/wp-content/uploads/2022/08/POA-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-08-10 09:17:292024-11-13 11:15:57What is a Power of Attorney in Pennsylvania? https://cornerstonelaw.us/wp-content/uploads/2022/06/Beneficiary-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-06-08 09:51:402023-05-05 10:05:03Giving Notice to Estate Beneficiaries

https://cornerstonelaw.us/wp-content/uploads/2022/06/Beneficiary-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-06-08 09:51:402023-05-05 10:05:03Giving Notice to Estate Beneficiaries https://cornerstonelaw.us/wp-content/uploads/2022/05/Estates-sunset-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-05-16 09:55:082024-11-13 11:18:42Opening an Estate in Schuylkill County

https://cornerstonelaw.us/wp-content/uploads/2022/05/Estates-sunset-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-05-16 09:55:082024-11-13 11:18:42Opening an Estate in Schuylkill County https://cornerstonelaw.us/wp-content/uploads/2022/02/Death-certificate-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-02-07 15:24:012023-05-05 10:43:38Why You Can’t Photocopy Pennsylvania Death Certificates

https://cornerstonelaw.us/wp-content/uploads/2022/02/Death-certificate-header.webp

670

1760

Cornerstone Law

https://cornerstonelaw.us/wp-content/uploads/2017/06/cornerstone-law-black-300x109.png

Cornerstone Law2022-02-07 15:24:012023-05-05 10:43:38Why You Can’t Photocopy Pennsylvania Death Certificates